ECB and EBA publish joint report on payment fraud

1 August 2024

- Total value of fraud across main payment instruments at €4.3 billion for 2022 and €2.0 billion for first half of 2023

- Report confirms effectiveness of strong customer authentication requirements, in particular for protecting against card fraud

- Card fraud risk lower for transactions within the European Economic Area, owing to mandatory application of strong customer authentication

The European Central Bank (ECB) and the European Banking Authority (EBA) today published a joint report on payment fraud. The report assesses payment fraud data reported semi-annually by payment service providers across the European Economic Area (EEA) for a variety of payment instruments, such as credit transfers and card payments.

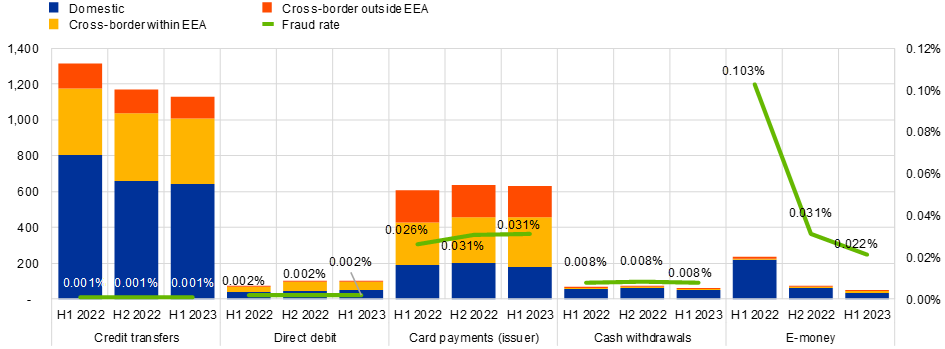

The total value of fraudulent credit transfers, direct debits, card payments, cash withdrawals and e-money transactions in the EEA amounted to €4.3 billion in 2022 and €2.0 billion in the first half of 2023. Most payment fraud in terms of value was related to credit transfers and card payments, while card payments also accounted for most in terms of volume. In the first half of 2023, card fraud with cards issued in the EEA accounted for 0.031%[1] of the total value and 0.015% of the total number of card payments. Similar fraud rates were observed for e-money transactions (0.022% in value and 0.012% in volume). Fraud rates were substantially lower for other instruments, in particular for credit transfers (0.001% in value and 0.003% in volume).

Absolute and relative levels of fraud by type of payment instrument

(left-hand scale: total value of fraud (EUR millions); right-hand scale: value of fraud as a share of the value of transactions)

Source: EEA payment service providers (excluding those from Liechtenstein where the reporting reference period only started in the second half of 2022).

The report confirms the positive impact of the strong customer authentication (SCA) requirements that were introduced under the revised EU Payment Services Directive (PSD2) and the supporting technical standards that the EBA issued in 2018 in close cooperation with the ECB. SCA-authenticated transactions displayed lower fraud rates than non-SCA transactions, especially for card payments. Furthermore, fraud rates for card payments were ten times higher when the counterpart was located outside the EEA, where the application of SCA is not legally required.

The report also finds that losses stemming from payment fraud were distributed differently among liability bearers, depending on the instrument or country. Most card fraud (71% of total value in the first half of 2023), along with a large share of credit transfer and direct debit fraud (43% and 47% respectively) involved cross-border transactions.

More details can be found in the full report.

For media queries, please contact Nicos Keranis, tel.: +49 172 758 7237.