Malaysia: A Flourishing Fintech Ecosystem

Malaysians have embraced financial technology; commonly used forms of fintech in the country include digital payments and mobile wallets (photo: iStock/Jimmy Fam)

February 28, 2020

Financial technology, or fintech as it has come to be known, gets a lot of attention for its extraordinary potential to change lives and change economies. Fintech can help ordinary people access financial products securely and efficiently, while boosting countries’ economic growth.

In Malaysia, where annual economic growth has averaged just under 5 percent over the past five years, fintech is a part of everyday life. It is rapidly becoming a central part of the country’s financial sector, with considerable promise for expansion, according to new IMF analysis.

With its growing middle class, high mobile phone penetration rates, and strong government support for the digital economy, Malaysia is well situated to take advantage of fintech innovation. From mobile wallets and electronic payments, to crowdfunding and “insurtech” (the combination of insurance and technology), Malaysian businesses and consumers appear ready to embrace the technology.

Internet banking in Malaysia has quadrupled in the last decade, topping a 90 percent usage rate in 2018. Mobile banking is also booming, supported by near-universal 4G network coverage, affordable data, and 5G is in the works. It’s no coincidence the World Economic Forum’s 2019 Network Readiness Index ranked Malaysia high among the 139 countries surveyed—ahead of Italy, China, and Chile—and first among countries in emerging and developing Asia.

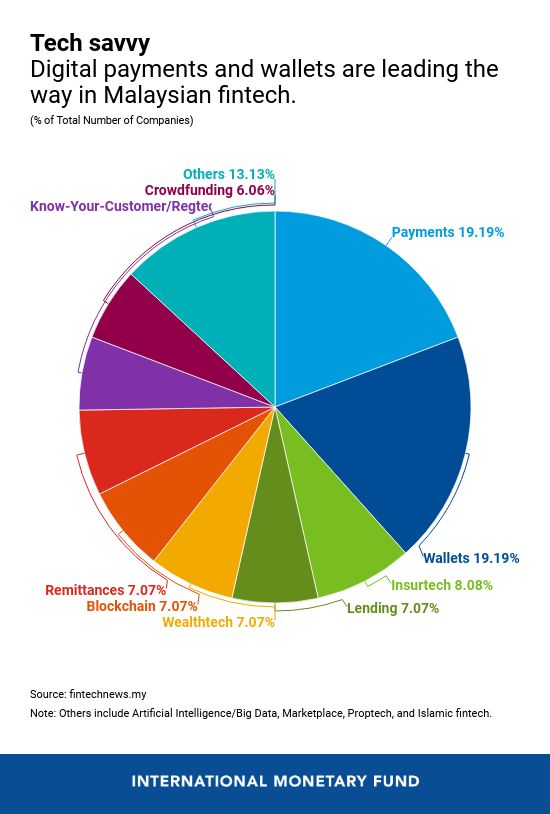

Where’s the money?

The most commonly used forms of fintech in the country are digital payments and mobile wallets, followed by “insurtech,” lending, digital remittances, blockchain, crowdfunding, electronic Know-Your-Customer processes, and other forms of financial technology.

Developments in Malaysian fintech are altering the country’s financial sector landscape. For example, while fintech products offered by traditional financial institutions expand, the number of physical commercial bank branches is declining, and the number of automated teller machines has fallen over the last two years. Traditional Malaysian banks continue to dominate in deposits, lending, and raising capital while, at the same time, adopting new technologies and either competing or collaborating with new tech startups. As of April 2019, there were close to 200 startups in Malaysia in a range of fintech areas, including payments, lending, and blockchain.

Road ahead

Of course, the rapidly evolving technology—alongside new consumer habits—is not without risk or challenges. Malaysia has been a leader on regulations to ensure that the financial system remains safe amid the possibility of cybersecurity incidents. Well aware that cyberattacks can undercut customer confidence and inflict widespread damage, Malaysian banks and regulators list cybersecurity among their issues of top concern.

Additional challenges to future fintech growth in Malaysia, for both financial institutions and new fintech businesses, include a shortage of talent in key tech areas like data analytics and machine learning, regulatory burdens, and access to funding.

As a leader in Islamic finance, Malaysia has a unique position within Islamic fintech, according to IMF analysis. Islamic bank loan growth in the country expanded by 8.9 percent in 2018, compared to 2.5 percent for conventional banks. While Islamic fintech is still in its infancy in Malaysia, the central bank supports efforts to promote the sector. Islamic financial institutions can benefit from fintech in many of the same ways that conventional finance does. Some fintech tools could be particularly useful in Islamic finance, since improved transparency—a core principle of Islamic finance—could be a result.